By Ian Richards, Senior Vice President, Borrower Analytics Group | January 2026

Our clients and readers know that there is considerable heterogeneity within the GNMA sector, which is dominated by FHA-insured and VA-guaranteed loans. These differences include average balance, credit characteristics, LTV, and other attributes.

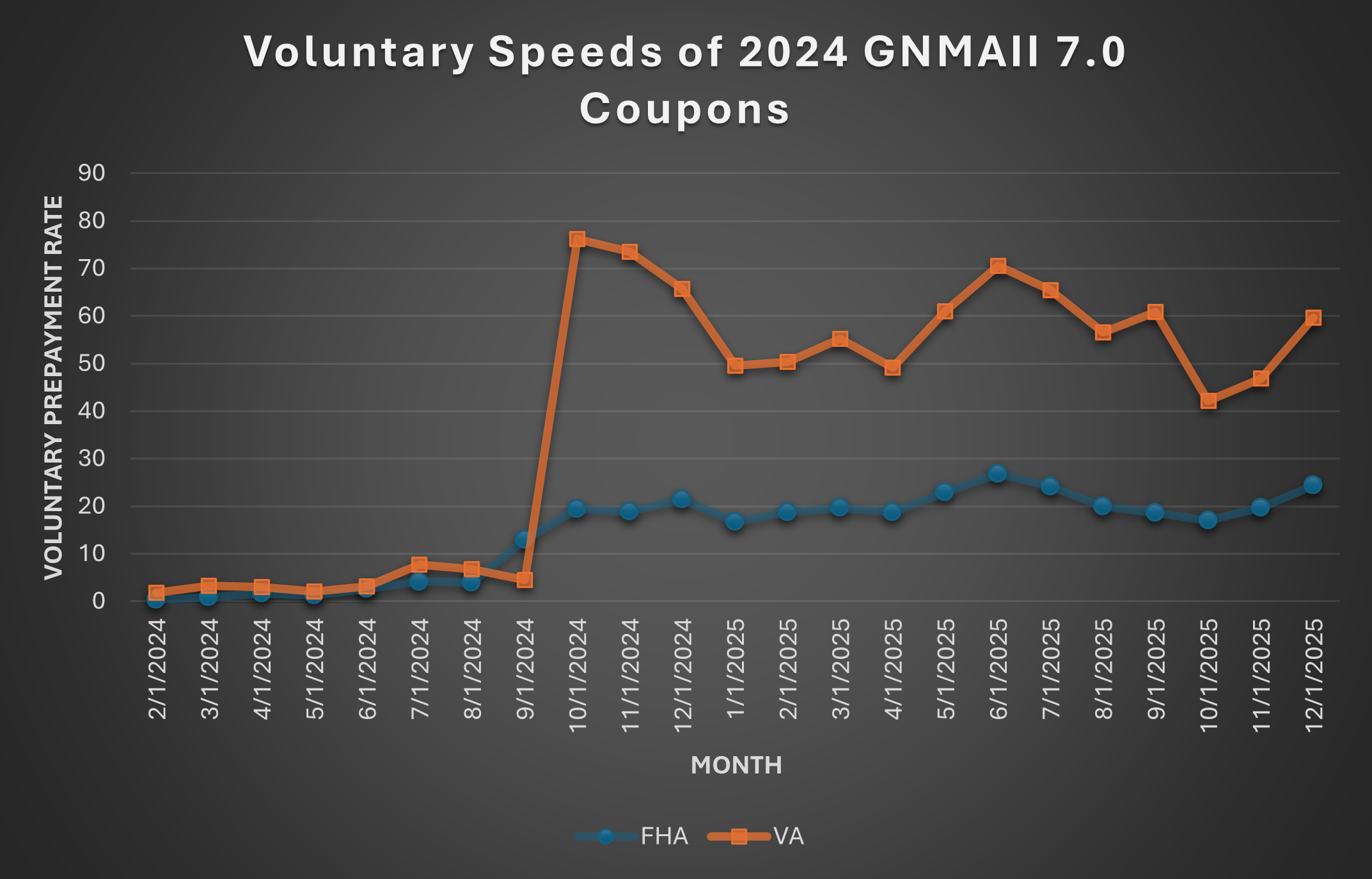

While VA loans have always been more sensitive to rate incentives, balance effects, and age, that sensitivity gap has widened dramatically over the past couple of years. The graph below displays the gap in annualized voluntary speeds within GNMA 7.0 coupons from the 2024 vintage.

While both FHA and VA loans within this vintage/coupon cohort are in the money, dispersions in balances, rate incentive sensitivity, and age curves result in VA speeds being 2-3x faster. Further, these differences cannot be explained by VA attributes (such as higher balances and better credit). It is obvious that this disparate behavior has important implications for valuations (OAS) and risk management (OAD) across the GNMA landscape.

For more than 35 years, MIAC has modeled FHA and VA loans as distinct segments for both prepayment and credit. Recent prepayment behavior reinforces the importance of maintaining this analytical separation when evaluating GNMA portfolios.

Additional analysis and discussion will be available in future MIAC Perspectives. To receive future perspectives, white papers, and market updates, subscribe here: https://miac.interactmarketing2.com/email-newsletter-subscription-miac-analytics/

We welcome feedback and discussion. For more information, please contact Ian Richards at Ian.Richards@miacanalytics.com or your MIAC representative.